Editorial

The Private Sector dialogue with the Prime Minister of Bangladesh, H.E. Sheikh Hasina Wajed was well attended by the Malaysian business leaders. The lively exchange of Questions and Answers revealed that there were ample business opportunities in many sectors in Bangladesh. Bangladesh is certainly on the investment and business radar of our Malaysian companies. H.E. Sheikh Hasina Wajed gave her Government’s assurance to assist and expedite the realisation of Malaysian investments in her country which has a population of 150 million. Members are encouraged to look more closely at this burgeoning market. The Bangladesh-Malaysia Chamber of Commerce Industry (BMCCI) is ready to assist our members to make any significant inroads.

In this edition, we also feature Zambia. The untiring efforts of YBhg Dato’ J. Jegathesan, MASSA’s EXCO member who is currently the Senior Economic Advisor for JICA and Government of Zambia, have yielded much fruit in bringing Malaysian investments to Zambia. The Deputy Minister of the Ministry of Finance and National Planning of Zambia, the Honourable David Phiri led a delegation of Government officials to Malaysia to meet potential Malaysian investors on 26 July 2010. The Honourable Deputy Minister also called on YBhg Tan Sri Azman Hashim, President of MASSA at his office. We wish to also acknowledge with thanks the article on Zambia contributed by His Excellency, Anderson K. Chibwa, the High Commissioner of Zambia to Malaysia.

We are pleased to welcome the article from the Ministry of Natural Resources and Environment, Malaysia. We look forward to feature more articles especially the Ministry’s programmes in support of the initiatives to “Go Green”. Malaysian companies are well placed to tap on the emerging business opportunities in this new sector and even take it cross border to the countries of the South.

To the new members of MASSA, we wish to take this opportunity to extend a warm welcome to each of them. We look forward to all our members’ active participation in MASSA’s activities, programmes and to use this platform to maximise their south-south connections.

Last but not least, allow me to use this occasion to wish all our Muslim members and friends, “Selamat Berpuasa” and “Salam Aidil Fitri”.

Fatimah Sulaiman

Editor

Forthcoming Events

1. Intrade Malaysia 2010 at MECC, Kuala Lumpur, 9 – 11 November 2010.

2. Global Expo Botswana (2010), 17 – 20 November 2010.

President’s Message

Despite the global challenge and uneven recovery, Asia is expected to remain relatively stable compared to its counterparts in Europe and the United States. Asia’s growth is largely fuelled by steady domestic demand and a healthy banking sector.

In Malaysia, while the economic fundamentals have improved with an impressive 1st Quarter of 2010 GDP growth of 10.1%, we will need to be vigilant to the continuing contagion risks and external headwinds given the challenging global outlook. Nevertheless, Malaysia GDP growth for 2010 should be at 7.0% to 8.0% which is commendable.

Much has been said about the drop in FDI inflows to Malaysia. In 2009, FDI inflows in Malaysia fell 81.1% to US$1.38 billion from US$7.32 billion in 2008. Outflows fell 46.4% to US$8.04 billion from US$14.99 billion. This evidently shows that there is a very competitive environment for FDIs set against a difficult external climate. We are heartened to note that our Government is seriously addressing this issue, namely to create an enabling environment to facilitate trade and promote investments. The New Economic Model (NEM) and the Government’s Economic Transformation Programme seek to address the structural issues afflicting the Malaysian economy and to ultimately create a conducive business environment to enable private sector investments to take the lead role in injecting greater momentum and dynamism into the Malaysian economy.

We must emerge stronger and more competitive. For this to happen, Corporate Malaysia must work hand-in-hand with our Government to create a winning formula to regain this competitive edge to attract domestic and foreign investments. These investments can, in turn, be strategised to enhance our economic linkages with the South-South countries.

I have pleasure to welcome on-board YBhg Tan Sri Ghazzali Sheikh Abdul Khalid and YBhg Dato’ Cheah Sam Kip, the new executive committee members of MASSA. I also want to thank all committee members for their continuing support and commitment.

In line with the festive season, I take this opportunity to wish all our Muslim members and readers “Selamat Hari Raya Aidil Fitri, Maaf Zahir Batin”.

TAN SRI AZMAN HASHIM

President

Diary Of Events

MASSA & TEAM “Monthly T3 Get-Together”, 21 September 2010

MASSA and TeAM jointly organised a “TeAM Monthly T3 Get-Together” event in Bangsar, Kuala Lumpur for MASSA members. The speaker of the event was Mr Harvinder Singh, Founder of InControl-Tech, a specialist in process control and communications systems that provides the Control and Communications Systems for SMART Tunnel, one of the longest multi-purpose tunnels in the world.

MTCP Programme at Menara MATRADE, Kuala Lumpur, 14 October 2010

MATRADE organised the Malaysian Technical Cooperation Programme (MTCP) entitled “Interfacing with Chambers of Commerce on Global Challenges and Trade Opportunites” for Chambers of Commerce from developing countries from 12 to 21 October 2010. Ms Ng Su Fun, Executive Secretary of MASSA and General Manager of MASSCORP Bhd, presented a paper on MASSA and MASSCORP Bhd’s objectives, functions and activities to the 17 participants from 15 developing countries who participated in this programme.

Courtesy call on MASSA President by Ambassador of the Republic of Uruguay, 18 October 2010

H.E. Gerardo Prato, Ambassador of the Embassy of the Republic of Uruguay to Malaysia, made a courtesy call on YBhg Tan Sri Azman Hashim, President of MASSA, at his office. Mr Jaime Pache, Counsellor and Deputy Chief of Mission from the Embassy of the Republic of Uruguay accompanied His Excellency at this meeting.

(2nd from left) Tan Sri Azman Hashim, President of MASSA with (right) H.E. Gerardo Prato, Ambassador of the Republic of Uruguay to Malaysia and (left) Mr Jaime Pache, Counsellor and Deputy Chief of Mission from the Embassy of Uruguay

Courtesy call on MASSA President by Pakistan High Commissioner,

4 November 2010

YBhg Tan Sri Azman Hashim, President of MASSA also received a courtesy call from H.E. Masood Khalid, High Commissioner of the High Commission for Pakistan to Malaysia at his office. Mr Wajihullah Kundi, Commercial Counsellor of the High Commission for Pakistan to Malaysia accompanied His Excellency at this meeting.

(2nd from left) Tan Sri Azman Hashim, President of MASSA with (2nd from right) H.E. Masood Khalid, High Commissioner of Pakistan to Malaysia, (1st from left)

Mr Wajihullah Kundi, Commercial Counsellor of the High Commission of Pakistan and Ms Ng Su Fun, Executive Secretary of MASSA

4th INTRADE MALAYSIA 2010 at MECC, Kuala Lumpur, 9 – 11 November 2010

MASSA participated in the 4th International Trade Malaysia Exhibition (INTRADE Malaysia 2010) organised by MATRADE at the MATRADE Exhibition & Convention Centre (MECC), Kuala Lumpur. This year’s exhibition, themed “One World, One Marketplace”, was officially opened by YB Dato’ Sri Mustapa Mohamed, Minister of International Trade and Industry, Malaysia.

Running concurrently with this exhibition were notable highlights such as the Incoming Buying Mission (IBM) Buyers-Sellers Meeting held on 8 and 9 November 2010, the 4th KL International Trade Forum 2010 (KLITF) on 11 November 2010 and the FTA @ INTRADE Programme, an initiative to promote the utilisation of FTA concessions to increase international trade for exporters to gain a competitive advantage in the global marketplace, etc.

Visit to Sunway Medical Centre by a group of 20 doctors from various hospitals in China, 6 December 2010

MASSA facilitated a study visit to Sunway Medical Centre by a group of 20 doctors from various hospitals in China. These doctors are part of the International Medicine Study and Exchange Association (IMSEA).

Limkokwing: The University Of The Future

In the 21st century, change comes fast and furious. For many organisations, it requires a mindset that is extraordinarily alert, savvy with the latest technology, relentless in seeking new solutions and courageous in undertaking incredible risks for rewards that benefit the world. The future has always been defined by the power of imagination. It has always been about pushing back the boundaries and breaking down the barriers. It has always been about pushing the limits, rewriting the rules and charting new frontiers.

Three decades of nation building, industry transformation and talent creation

Since the 1970’s, we have been transforming the way people think and do things. We began as a company focused on strategic communications in Malaysia, helping improve the country’s foreign direct investment, trade promotion, country branding and international relations and addressed a host of socio-economic issues that required campaigns to change mindsets and move people forward. We believe in the talent of people and their ability to perform. Midway through our journey, we ventured formally into higher education as we saw a meaningful role in creating the right kind of human capital for the world.

World’s only university focused on applied creativity and industry innovation

The Limkokwing ethos is a creative, stimulating place that does not fit into any mold of what a university should be. This is a dynamic, multi-cultural congregation of young, enthusiastic creative minds, supported by experienced faculty and industry professionals. The Limkokwing eco-system manages change through the driving force of its Founder President with the support of a global team. It operates in a pressurised environment that overturns traditions and whenever possible re-engineers its delivery to enable the university to stay relevant to market demands and industry trends.

Industry within a university learning environment

We don’t follow the norm because it is out of sync with the pressures and demands of today’s lifestyle. We engage in what is called “blue sky, green field thinking” to produce a university that looks at how young people need to be educated. We face many obstacles, especially from those who have fixed ideas about education. But we have continued to move forward, pushing past the boundaries because of the encouragement we continue to receive. Industry – which benefits from our efforts – has always welcomed our ideas and organisations like the World Bank and UNESCO have shown interest in our methodology.

Creating a culture for entrepreneurial development and industry leadership

We encourage entrepreneurship, as the world is moving into a new era of greater connectivity and web networking. The advanced skills that our graduates gain at the University, encourages them to set up their own businesses offering services in these new developments. Being technology driven we try to keep up with new developments in both software and hardware. This is necessary to sustain the individual’s relevancy in the marketplace. Technology is leaping into an age of advancement that will see industry moving completely away from traditional methods and adopting new infrastructure for global computing.

Merging the best of East and West

Limkokwing University’s Best of East and West strategy is to bring both sides of the world together in a way that will enable young people to build their knowledge of other cultures. Now with the rise of China and India, we can look forward to a fusion of the best of the East and West that will take the world to a new level of knowledge and discovery.

Highly motivated, skilled, adaptive, competitive, enterprising, tech-savvy creative thinkers

The Limkokwing eco-system is developing a new class of knowledgeable, tech-savvy, culture-sensitive, global-trend-savvy graduates. This graduate is resilient, adaptable, innovative and at home in the technology-led 21st century. He or she carries a level of understanding and maturity that comes only from experience and exposure to multiple cultures and ideas. Thousands of our graduates are now employed in entrepreneurial pursuits or engaged in content development.

12 campuses in 7 countries and partners with 282 universities/colleges from 77 countries

Our global network of campuses and university partners provides students with the widest selection of places where they wish to conduct their research or complete their degrees. Our award-winning university website has attracted 108 million visitors from 195 countries, making it one of the world’s most popular university websites.

Virtual, technology-driven, creativity-focused worldwide operation that conducts productive R&D and applied innovation

Our vision for global education is increasingly getting responses from people, governments and institutions across the world. We are inextricably linked with the future of the countries we are located in. Our deep involvement in building human resources puts us in a position of great responsibility because the future of the world rests on the abilities of the next generation.

We have become a global community with shared experiences and shared values. Our alumni are actively engaged in growing the productivity of companies and improving the effectiveness of organisations. In the near future we will not be surprised to see our alumni in influential positions. By doing what we are doing now, we reach into a future to effect change through the enhanced knowledge, cultural competency and skills of our graduates.

We will be an expanded organisation as we establish ourselves in more countries.

We will be an interactive virtual campus and through this facility we will reach millions more who cannot wait for the development of our mortar and stone structures.

We will change education to become more practical and useful to impoverished communities.

We will transform the world through the knowledge and talents of the next generation.

Country Feature – Colombia: The Skillful Tiger The First 100 Days: A Taste Of What’s Next!

Last November, Colombia’s new president Juan Manuel Santos marked his first 100 days in office. Although the road to complete security and economic growth has been largely paved by previous President Alvaro Uribe, the future ahead looks promising indeed if everything that has happened in the last 100 days represents just a few stripes of the tiger.

Evidence of progress may be marked by the efforts within a country but more so are the actions from the outside world. Every industry sector will have a chance of getting a new lease of life. Every challenge is being assessed and pro-actively dealt with, using the assertiveness of a tiger and the gentleness required to achieve success at all levels.

The presentation of the National Development Plan 2010 – 2014 by the Colombian government in November was commemorated by President Juan Manuel Santos with the declaration: “We will realise our dream to transform Colombia into a developed nation!”

The big picture: be part of us … we want to be part of you!

While business-to-business activities are essential to a country’s development, the underlying strengths within the big picture are the trade agreements between nations. Here, Colombia has seriously considered long-term strategies and those already in place are evidence of it. In anticipation of the Free Trade Agreement with Canada, investors from that country are pouring in. The FTA with the USA is in its final stages and Colombia’s efforts to strengthen those within Latin America will ensure that the country becomes a strategic location from which to do business.

Under the new leadership, staying within the region or within the traditional market of Europe will be too short sighted. After being given a two-year seat within the UN Security Council, Colombia has requested to be part of APEC and wants to secure further Free Trade Agreements with countries in Asia apart from the ones it already has with India and Korea.

Breaking mental geographic borders is high on everybody’s mind and Southeast Asia is one of the targeted destinations.

Powerful Attractions

- Secure environment

- Growing economy

- Political stability

- 4th largest economy and 3rd largest population in South America

- Strategic location

- Large market of 45 million people

- Highly educated and performance driven society

- Strong legal framework for investment

Deadline 2014

- Economic growth with an average of 6.2% per year

- Take 2.5 million people out of poverty

- 1 million additional school places

- 50% of the population connected to the Internet

- Return land to 160,000 original landowners

- Develop a world-reaching agro-industry

- Reach total exports worth US$52.6 billion

- Generate US$13.2 billion in foreign investment

- 1 million new homes

Size, Variety, Knowledge & Drive

A country almost three times the size of Malaysia, Colombia has vast opportunities. Although Bogotá’s population of about eight million people may rival other capital cities, Colombia’s other main cities of Medellin, Cali and Barranquilla boast huge populations. No other country in Latin America has such large population clusters.

Colombia has the potential to become a fully self-sufficient country. In addition to its high-technology industries and favourable prospects of becoming an agricultural powerhouse, Colombia also has growing oil & gas reserves and valuable deposits of minerals.

Beyond just having access to raw materials, continuous research activities ensure that relevant knowledge is obtained to maximise the use of the materials as well as protect the environment.

Economic activities that are shaping the future

After eight years, Lufthansa, the German airline, made Colombia its aviation hub for South America. In a competitive and complex global market, a decision like this goes far in establishing a positive picture of the country as a promising investment hub and augurs well for its future.

As its supply of oil, gas and minerals increases, Colombia will become even more attractive to global economic giants such as India and China. When the world saw a 4% decline in tourism in 2009, Colombia recorded a 10% increase, thanks to its natural wonders and tourist-friendly environment. Factors like these and others are key to shaping the future of Colombia today.

Managing the environment: values beyond doing business

Colombian society in general shows a pro-active, caring attitude in using the country’s abundant natural resources without ever abusing it. These values are also reflected in the Government’s commitment and focus in promoting such activities. Bio-energy, huge plantations and the direct and indirect effects of their activities on the environment, are high on the priority list. It is here where Malaysia can share and guide the massive agricultural plans of Colombia. Driven by Research & Development as the key driver for sustainable growth, the opportunities

are endless.

“Opportunity has its own voice and the world is listening to Colombia.”

Malaysia and Colombia: merging the best of both worlds

Malaysia and Colombia can become powerful economic allies. Malaysia is an excellent example and role model due to its remarkable progress in becoming a developed nation; which is ultimately Colombia’s aspiration.

Malaysia and Colombia can become powerful economic allies. Malaysia is an excellent example and role model due to its remarkable progress in becoming a developed nation; which is ultimately Colombia’s aspiration.

In terms of investors, Colombia has many of them ready. Facing the Pacific Ocean, the country offers easy access for exports from Malaysia. The new airport of El Dorado in Bogotá is considered to be the next regional hub for both passengers and cargo – the logistics key to success.

Politically, both countries have always had very positive ties. During the leadership of Tun Mahathir, several business missions from Malaysia explored opportunities in Colombia. After these visits, the worries that most Malaysian investors had over security issues in Colombia began to disappear.

This article was co-written by the Honourary Consul of Malaysia in Colombia, Dr Arturo Infante Villareal and Peter Jähne from Quest Corridor.

| Business Exploration Visit To join a business delegation to Colombia in March/April 2011, please contact MASSA. |

Contact Details • artuinfante@gmail.com • peter@questcorridor.com |

UNCTAD – The Least Developed Countries Report 2010

The Least Developed Countries Report 2010 by UNCTAD was launched in Kuala Lumpur, Malaysia on 29 November 2010, by Mr Kamal Malhotra, United Nations Resident Coordinator for Malaysia and presented by Datuk

Dr Zainal Aznam Mohd Yusof, Council Member, National Economic Advisory Council (NEAC).

Mr Malhotra said, “The UN recognises the special needs of the LDCs and since 1971 has denominated “Least Developed Countries” (LDCs) a category of States that are deemed highly disadvantaged in their development process, many of them for geographical reasons, and facing more than other countries the risk of failing to come out of poverty. As such, LDCs are considered to be in need of the highest degree of attention on the part of the international community.

UNCTAD’s The Least Developed Countries Report provides a comprehensive and authoritative source of socio-economic analysis and data on the world’s most impoverished countries. It outlines the most critical issues, challenges and risks our region faces. The Report is intended for a broad readership of governments, policy makers, researchers and all those involved with LDCs’ development policies.”

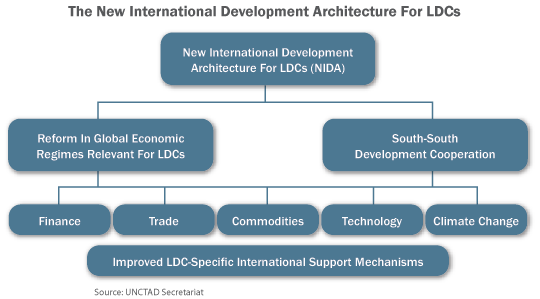

The Least Developed Countries Report 2010 is subtitled “Towards a new international development architecture for LDCs”. The objectives of the proposed new international development architecture are:

- Reversing the marginalisation of LDCs in the global economy and helping them in their catching-up efforts, in particular by helping them to develop their productive capacities – that is, their abilities to efficiently and competitively produce an increasing range of higher value added goods and services through expanding investment and innovation;

- Supporting a pattern of accelerated economic growth to improve the general welfare and well-being of LDC populations; and

- Helping LDCs graduate from LDC status (only two countries, Botswana and Cape Verde, have done so in the last 30 years).

“Business as usual” isn’t working, the report argues. A number of LDC-specific international support measures have been devised to promote the economic development of these nations, but the UNCTAD study concludes that they have had largely symbolic, rather than practical, development effects. In the majority of cases, the report contends, they have not promoted the development of productive capacities, and the lack of these capacities is the key source of the structural economic weaknesses of LDCs.

Mr Malhotra said, “LDCs have remained marginal in the world economy owing to their structural weaknesses and the form of their integration into the global economy. Unless both these aspects are directly addressed, they will remain marginal and their vulnerability to external shocks and pressures will persist.

Unfortunately, existing special international support measures for LDCs do not effectively address the structural weaknesses of these countries or how the LDCs interact with the global economic system. Therefore it is hardly surprising that during the past three decades, only two countries were able to graduate from the LDC status and in fact the number of countries falling in the LDC category has doubled.”

The report says LDC governments must play stronger roles in creating favourable conditions for capital accumulation, technological progress, structural transformation – especially a shift away from LDCs’ dependence on commodity exports – and the creation of productive jobs that are vital for substantial poverty reduction. The new international development architecture should support these national efforts.

A feature of the proposed architecture is that it expands the focus beyond aid and trade to include technology, commodities and climate change as key pillars. The proposed new international development architecture thus includes reforms in global economic regimes in these areas which directly affect development and poverty reduction in LDCs. It encourages the design of a new generation of special international support mechanisms for LDCs that would address their specific structural weaknesses. Efforts to enhance South-South development cooperation are also recommended.

“The Report calls for a new generation of LDC-specific international support mechanisms that should be accompanied by resources, including financial resources, institutions, policy frameworks and organisational entities, to enable their implementation. They should move beyond a focus on trade and market access, to promote development of productive capacities in LDCs.

Only then can the International Support Mechanisms (ISMs) be actionable and potentially address the specific structural weaknesses and vulnerabilities of LDC economies today, including: weak human resources, poor physical infrastructure, low technological capabilities, excessive dependence on external sources of growth, low share of manufacturing in GDP and high levels of debt.

It requires the State to play a more developmental role in creating favourable conditions for capital accumulation, technological progress and structural transformation, as well as in the generation of productive employment opportunities, which is the key to substantial poverty reduction in the LDCs,” added Mr Malhotra.

The report proposes an agenda for action to create a new international development architecture for LDCs.

It identifies five major pillars:

- In the area of finance, the report calls for increased official development aid inflows in line with the Organisation for Economic Cooperation and Development (OECD) – Development Assistance Committee (DAC) aid commitment of 0.15 and 0.20 per cent of gross national income (GNI) and enhanced efforts to enable country ownership of national development strategies. It argues for increased use of aid to support domestic resource mobilisation as well as for innovative uses of aid to develop productive capacities.

- In the area of trade, the report suggests that the so-called “early harvest” of measures (such as full duty-free, quota-free market access for all LDCs and more favourable treatment of services trade from LDCs) benefiting LDCs that have already been agreed upon in the Doha Round of world trade negotiations should not be made contingent on completion of the negotiations. The report calls for empowering LDCs to use existing flexibilities under current trade rules so that they can implement strategic trade policies, as well as more efficient delivery of aid for trade.

- In the area of commodities, an absence of global governance appears to be the main obstacle to greater stability in prices and earnings. Priority actions in the global economic regime should include the introduction of new measures for reducing the volatility of commodity markets and the adverse impacts of this volatility. Moreover, improved management is proposed to increase returns for LDCs – and alleviate financial and fiscal bottlenecks – from the harvesting of their natural resources.

- In the field of technology, the report calls for a new, coherent, and dynamic pro-development knowledge architecture centred on LDC technological needs and capabilities. In particular, the report calls for a reorientation of global governance on technology and intellectual property rights. It proposes a series of international support mechanisms, including the development of a technology license bank and a multi-donor trust fund for financing enterprise innovation in LDCs.

- In the area of climate change, the report calls for urgent and adequate financing of the LDC Fund in the field of climate change, and improved access for LDCs to the United Nations Framework Convention on Climate Change’s Clean Development Mechanism as a means of overcoming the financial barriers that prevent LDC access to renewable energy technology.

South-South development cooperation is considered relevant to all five of these issues. In 2007-2008, developing countries were the source of 62 per cent of LDC merchandise imports and the destination of slightly more than half of their merchandise exports. There are further opportunities for expansion of trade, technology and investment flows between LDCs and other developing countries, as well as exchange of policy experiences, the report says. These opportunities should be seized.

The forward-looking agenda UNCTAD proposes would create a much more supportive international environment for LDCs. Linking international support mechanisms for LDCs with a new international policy and cooperation framework that can deliver a more stable, equitable and inclusive global governance regime for all countries is one of the most urgent challenges facing the international community, the report contends. Doing so will not only help make special international support for LDCs more effective, it will also contribute to including LDC issues in wider international activities and debates on development.

“The UNCTAD LDC 2010 Report will contribute to an increased appreciation and understanding of the complexities of the LDCs economies and their future role in ensuring a more dynamic, sustainable, and equitable growth trajectory that supports more inclusive human development. The Least Developed Countries Report 2010 will be used to help inform debate at the Fourth United Nations Conference on Least Developed Countries scheduled for May 2011 in Istanbul (Turkey). That conference will result in an international plan of action intended to address the needs of LDCs over the next decade,” concluded Mr Malhotra.

One billion people will be living in LDCs by 2017, the report notes. It says they need to find new development paths which will reduce their marginalisation in the global economy and will substantially reduce their poverty.

Country Feature – Ecuador: A Gateway For Doing Business In South America

OVERVIEW

Due to its privileged geographical position, the safety offered, a solid legal framework, a favourable performance of the economy – which according to figures of the Economic Commission for Latin America and the Caribbean (ECLAC), is among the best in Latin America – and its modern physical infrastructure and road network, as well as the openness and responsibility of the Government of President Rafael Correa in promoting investment under clear rules; Ecuador welcomes foreign investment in areas that are considered to be of strategic importance to the country’s economy.

A total of USD4.546 million have been invested in the Strategic Sectors between 2007 and 2009: USD3.077 million for Oil and Gas; USD554.60 million for water resources; USD474 million for Electricity and USD441 million for Telecommunications.

Firm and sovereign steps guide us forward. A sample of this is the signing of the contract to finance the hydroelectric project Coca-Codo Sinclair with China’s EXIMBANK for a total of USD1.682.745.000. This will allow us to transform into a reality, the largest infrastructure project in the country that will generate 1.500 MW and energy of 8.600 GW-hour per year to cover 35% of our energy demand. This is a true demonstration of the confidence that foreign investors have in Ecuador.

Ecuador lies on the equatorial line and limits to the north with Colombia, to the south and east with Peru, and to the west with the Pacific Ocean. There are four distinct geographical zones. The first one is the Andes’ highlands, which begins at the northern border with Colombia and ends at the southern border with Peru. The second region is the Coast, a coastal plain between the Andes and the Pacific Ocean. The third one is the Amazon made up by the upper basin of the Amazon River. The fourth one is the Galapagos Islands Archipelago, located 1,000km from

the continent, in the Pacific Ocean.

Ecuador has opened its doors to welcome foreign investment and relations of mutual benefit that will contribute to the country’s development and growth.

WHY INVEST IN ECUADOR?

Ecuador’s growing and stable economy, strategic location and logistical hub, mega diverse biological diversity, great human talent, access to Latin American and global markets, investor protection and incentives, as well as its U.S. Dollar economy, are but some of the strategic reasons to invest in the country.

Furthermore, Ecuador enjoys preferential access to the United States market through the Andean Trade Promotion and Drug Eradication Act (ATPDEA), which provides duty-free access for over 6,000 products. Ecuador also has an Economic Complementation Agreement with MERCOSUR that provides Ecuador with the potential to export approximately 4,000 products with no tariffs to Brazil and Argentina; and the European Union’s GSP PLUS provides Ecuador with the potential to export approximately 7,800 products with no tariffs to E.U. countries.

Public contracting processes are carried out through the National Institute of Public Procurement (INCOP), which articulates, harmonises and controls the execution of projects funded by public resources, through speedy procedures, transparency, efficiency and technologically-updated processes.

INCENTIVES FOR INVESTMENTS

Under a new legal framework known as the Production Code, foreign and domestic investments will be protected through an investment contract as an instrument to protect investors rights and to provide incentives and rules of engagement, such as: exemption from income tax on dividends and profits earned or distributed to companies (except tax havens) or non-residents of Ecuador; income tax exemption for first five years for new investments in strategic productive sectors; 100% additional reduction of labour costs from income taxes for first five years for new Investments in depressed economic development areas; reduction of 10% of income rate if enterprise re-invests in new assets or R&D (Rate of 12%); total exemption of 2% tax on foreign exchange outflows for international financing; additional deduction for income tax of costs of green and eco-efficient assets and machinery (if not mandatory by Authority); zero custom duties for capital goods imports; co-financing of Business Development Programmes to improve productivity and to promote exports; public development credit and risk capital at very competitive rates; exemption from capital gains, profits or income distributed by mutual funds, pension funds and commercial trusts; reduction of income taxes for companies from 25% to 22%; additional deduction for annual net increase in employment; deduction of lease payments for international trade of capital goods; accelerated depreciation (by request) on durable goods; zero tax on electricity produced and sold; among others.

BUSINESS OPPORTUNITIES FOR MALAYSIANS

The Official Visit to Malaysia from November 8 to 11 2010 by the Undersecretary of Trade and Investments of the Ministry of Foreign Affairs, Trade and Integration of Ecuador, Mr. Hector Eguez, and the General Manager of the Port Authority of Manta, Mr. Guillermo Moran; marked the first step in the implementation of a Sister-Port Agreement between the Port Klang Authority and the Port Authority of Manta, which could translate into the establishment of a strategic trade corridor and logistic hubs connecting Malaysia and the ASEAN countries to the South American markets through Ecuador.

In conjunction with the said visit, the Embassy of Ecuador in Malaysia, the Port Klang Authority and the Port Authority of Manta jointly organised the first Seminar on Business Opportunities in Ecuador, which was held on the 10th of November 2010 at the Concorde Hotel in Shah Alam.

This event confirmed the Ecuadorian Government’s desire to strengthen commercial ties with Malaysia, and the good turnout also evidenced the interest of Malaysian investors and businesses to seriously consider the prospect of making the most of the opportunities found in Ecuador.

The above-mentioned Seminar focused on specific opportunities for Malaysian investors in strategic Government projects such as: the components of the Manta-Manaus trade corridor project, which encompasses the development of Manta’s deep sea port (geographically the closest port to Southeast Asia in South America), Manta’s international airport, Special Economic Zones, the Refinery of the Pacific project (planned to become the largest oil refinery in South America) as well as the connecting roads and highways; Electricity Projects (Hydroelectric, Wind Power, Geothermic, Thermal, Transmission, Oil & Gas); Water Projects; Mining Projects; Oil and Gas Projects and Telecommunications Projects. These investment projects were presented with the Ecuadorian Government’s guidelines to present a bid, and the different contracting modes that apply depending on the type of project: Direct financing Government to Government, International Bidding with Financing, Strategic Alliances, Service Contracts, and Auction – Bidding.

Although the Seminar highlighted strategic investment projects in Ecuador, the Embassy and MASSA are planning for a Malaysian Trade Mission to visit Ecuador in 2011, which will include Malaysian businessmen interested in exploring for themselves the possibilities of importing Ecuadorian products to Malaysia, in addition to Malaysian investors. The Ecuadorian Government aspires that pioneering Malaysian businesses will play an intrinsic role in making Ecuador a logistic and trade Gateway to South America for Malaysia, the ASEAN countries and Asia.

For further information, please contact:

Her Excellency Lourdes Puma Puma

AMBASSADOR OF ECUADOR TO MALAYSIA

142-C Jalan Ampang, Wisma Selangor Dredging,

West Block, 10th Floor, 50450 Kuala Lumpur.

Tel : (603) 2163 5094 Fax : (603) 2163 5096

E-mail : embecua@po.jaring.my

Ministry Of Natural Resources And Environment Malaysia – The Hidden Economic Implications Of The Carbon Markets

Introduction

In response to the demand by developed countries, many developing countries are generating carbon credits for sale through the existing market mechanisms. However, these developing countries may unknowingly be selling their low-cost emissions reduction options and locking themselves into having to use higher cost options to accomplish their own emissions reduction pledges in the future. This article explores the role of the carbon markets in the context of current trends in multilateral climate negotiations and highlights the risk of rushing to cash-in low-cost emissions reduction credits.

Following the failure of the climate talks at the 15th Conference of the Parties (COP) to the United Nations Framework Convention on Climate Change (UNFCCC) in Copenhagen in December 2009, Parties began the arduous process of rebuilding trust in 2010. Through patient and delicate negotiations, Parties have managed to agree on a process that would take Parties through the crafting of a strategic set of COP decisions at Cancun, Mexico, with a view to achieving a legally binding agreement in Durban, South Africa at the 17th COP in 2011.

However, several disturbing trends have emerged in the negotiations. First, there are unambiguous signs that a significant number of developed country Parties no longer support a second commitment period (post 2012) to the Protocol. There are also signs that developed countries are distancing themselves from the principles of the Convention. Finally, there is a strong pressure for international carbon markets to play a greater role in future climate agreement regimes. These factors in combination paint a bleak picture of the future of an international multilateral climate policy as driven and influenced by developed countries.

A Protocol in peril

With two years remaining in the first commitment period (2008 – 2012) of the Protocol, it is evident that developed countries have had mixed success in achieving their emissions reduction targets. This has occurred in spite of the established flexibility mechanisms and the accounting loopholes in Land Use, Land Use Change and Forestry (LULUCF).

It is not surprising, therefore, that negotiations for the second commitment period of the Kyoto Protocol have been fraught with difficulty.

The US, having unfairly evaded commitments during the first commitment period, has maintained that it will have no part of the Kyoto Protocol, and that without a Congressional mandate; it will be unable to declare any more than a token emissions reduction pledge in any new legally binding agreement. Other developed countries, taking the cue from the US, are distancing themselves from the second commitment period of the Protocol and shifting the mitigation burden to developing countries. These collective positions and demands not only impact the functionality of the Protocol by decreasing the level of ambition of other developed countries, but also profoundly undermine the principles of the Convention.

A Convention in crisis

Also distressing is the developed countries’ gradual dissociation from the UNFCCC itself. This is because the principles of the Convention affirm the historical role of the developed countries as the primary emitters of greenhouse gases (GHGs) and differentiate countries according to common but different responsibilities. Furthermore, the Convention appreciates the priorities of developing countries to eradicate poverty and raise the living standards of their people.

Ultimately, the primary basis of the Convention is the link between development, wealth creation and the generation of GHGs, coupled with the fact that GHG emissions by the developed countries since the beginning of the industrial revolution are now affecting global climate and adversely impacting the lives of all peoples, particularly those least able to protect themselves from it. Some developed countries are now demanding that all Parties should have emissions reduction commitments, in effect, de-linking historical emissions of developed countries from our current climate predicament and shifting the emissions reduction burden to developing countries even while their per-capita emissions remain far below those of the developed countries. This will most certainly retard development, which, as mentioned above, is recognised as a priority under the Convention. Once again, these collective positions taken by the developed countries are unprecedented and clearly an attempt to subvert the principles of the Convention.

The current state of negotiations

In Cancun, the EU and the Environmental Integrity coalitions agreed to move firmly toward a second commitment period of the Kyoto Protocol, but only if the US and the rest of the Umbrella Group take on comparable reduction targets, and the major emitting developing countries implement emissions reduction actions. These positions support the Kyoto Protocol and Long-term Cooperative Action (LCA) tracks of the Bali Roadmap agreed to at COP 13 in Bali.

Regrettably, while developing countries were making major concessions on the LCA track, Japan and Russia, in a blatantly retrogressive move, announced that they would not be making emissions reduction pledges for the second commitment period of the Kyoto Protocol. These positions clearly oppose ambitious top-down emissions reduction commitments in favour of voluntary, bottom up emissions reduction pledges of the kind already being implemented by developing countries. In fact, they represent a step backward from the dismal pledges in the Copenhagen Accord, which, from a scientific standpoint, would already allow the increase in average global temperatures to exceed 2°C. Ultimately, the reason for this wish to dissociate from the Protocol and from the principles of the Convention stems from the link between emissions and wealth generation as discussed below.

The link between emissions and wealth generation

Unless we derive our energy from low-carbon fuel sources such as hydroelectric or nuclear power, productivity will most certainly be linked to emissions from the burning of fossil fuels. Even where stationary power sources are non-carbon related, we still use large amounts of fossil fuels for transportation. Therefore, granting a country emission rights is tantamount to granting increased productivity while restricting emissions will restrict productivity. From this standpoint the Protocol, with its legally binding commitments, imposes a significant burden on developed countries.

Faced with this prospect, developed countries would initially reduce non- GDP-linked emissions, followed by emissions marginally related to GDP, leaving emissions closely tied to GDP to the end. Further reduction in emissions would imply not just the specific cost of emissions reduction but also, the opportunity cost, a reduction in GDP, which would impact their economies. For this reason, developed countries have insisted on being allowed to accomplish further emissions reductions offshore, that is, through emissions reductions in developing countries. This, in effect, allows wealth generation to proceed unhampered in the developed countries while the emissions reduction is accomplished at much lower cost through emissions reduction credits that are generated in developing countries and purchased through the markets. If developing countries were not called to reduce emissions themselves, this situation would not be problematic, but the developed countries are already beginning to insist that developing countries should have emissions reduction commitments of their own.

As in developed countries, emissions reductions in developing countries also vary widely in cost. Ideally, developing countries should be implementing the lowest cost options for their own emissions reductions while assigning the higher cost emissions reduction options to be accomplished through financial assistance and technology transfer from developed countries as envisioned under the Convention. Instead, the allure of the carbon market is leading developing countries to use their low-cost mitigation options to generate low-cost emissions reductions for sale on the market when they might actually need these low-cost reductions to meet their own emissions reduction commitments now or in the future. Once these low-cost emissions reductions are sold, they are no longer available to the country to accomplish its own emissions reductions. The developing country will then have to rely on its higher cost emissions reduction options to reduce its own present and future emissions, almost certainly retarding economic growth and adversely affecting development. Meanwhile, the developed countries continue to generate wealth and economic prosperity through the unabated emissions of GHGs.

Avoiding ‘Double Duty Mitigation’

This ‘double duty mitigation’ by developing countries should be a concern to all developing country governments that are currently looking to ‘market mechanisms’ as a means of financing domestic emissions reductions. These market mechanisms represent the most efficient way of ensuring that economic growth remains robust in developed countries while taking advantage of market competition and the already lower cost of emissions abatement in developing countries.

In view of the aggressive marketing strategies of carbon credit brokers and buyers, developing countries, especially those that are already making voluntary emissions reduction pledges, need to be particularly concerned that their low emissions growth strategies take into account the need to ensure that sufficient low-cost mitigation options exist to achieve their own, self-financed emissions reduction pledges before embarking on the development of large-scale emissions reduction projects designed to generate voluminous carbon credits for sale in the competitive carbon markets. Enhancing awareness concerning this issue at all levels of both the public and private sectors will help governments avoid the negative impacts on development in a carbon constrained global economic environment.

3rd Quarter 2010 Update: Malaysian Economic Outlook

After a blistering pace in 1Q10, the global economy softened in 2Q10. This cyclical slowdown is expected to persist in 2H10, given weaker global trade conditions and the ongoing sovereign debt problem in the Eurozone. Nevertheless, developing Asia continued to lead global growth through their resilient domestic demand.

Similarly in Malaysia, economic growth decelerated to 8.9% yoy in 2Q10 on slower growth in net exports. Domestic demand was strong with private investment gradually recovering. All key sectors moderated, but were dominated by manufacturing and services. The industrial production index (IPI) up 4.0% yoy in Aug-10, despite a slower rate of growth in gross exports. The shipment of electrical and electronic products eased to 3.8% yoy in Aug-10 due to weaker global demand for chips. Meanwhile, non-electrical and electronic products were also down to 15.8% yoy, due to falling global commodity prices.

Headline CPI increased 2.1% yoy in Aug-10, due to the effects from lower subsidies on part of fuel and sugar. Meanwhile, core CPI was also firmer at 1.5% yoy in Aug-10. The banking system’s outstanding loan growth eased to 11.8% yoy in Aug-10, due to weaker demand from the business sector of 9.9%. Household loans growth continued to improve at a healthy rate of 13.4%. Total deposits in the banking system were unchanged at 8.7% yoy in Aug-10. Liquidity remained ample as indicated by the loan-deposit ratio of 77.4%, arising from a weaker mom growth in total loans compared to total deposits.

The 3-month net NPL ratio was steady at 2.1% in Aug-10, while the risk-weighted capital ratio (RWCR) was at 15.1%. These measures indicated that asset quality remained healthy and the capital base of the banking system was strong. The growth rate of broad money (M3) increased 8.2% yoy in Aug-10, due to higher credit demand, public spending, and foreign inflows. Narrow money (M1) accelerated by 13.9% on larger transactional demand ahead of the Eid celebration.

Using this data, MIER maintains its 2010 and 2011 economic growth forecasts at 6.5% and 5.2% respectively. Importantly, these forecasts are also supported by recent in-house surveys. The Business Conditions Index (BCI) fell sharply to 104.9 pts in 3Q10, which more than offsets the surge in the Consumer Sentiment Index (CSI) to 115.8 pts. Other indices also painted a similar gloomy environment ahead.

In terms of interest rates, MIER anticipates the OPR to be kept at 2.75% until end-2010. This is useful in order to assess the effects of previous rate hikes and the possible impact from the economic fallout in the Eurozone. The OPR will trend higher to 3.25% in 2011, in tandem with a higher overall CPI forecast of 2.5% yoy (2.2% in 2010).

Recent foreign exchange liberalisation measures have lifted RM sentiment and should be conducive for further development of the financial market. However, these measures also generated more volatility to exporters. MIER forecasts an average RM/USD of 3.20 in 2010 before strengthening further to 3.10 in 2011.

Editorial

In this edition, we are featuring two (2) neighbouring South American countries, namely Ecuador and Colombia which share quite similar demography and offer as yet untapped business opportunities for Malaysian entrepreneurs especially in the areas of infrastructure, construction and oil & gas. These two (2) countries also have ample natural resources to offer.

MASSA has plans to organise a business mission to these two (2) countries including Venezuela in 2011 to establish business linkages. Their respective Embassies in Kuala Lumpur are already working with us on an itinerary for the proposed mission. We look forward to members and your business associates to join us on this mission, tentatively planned for late April 2011. Do look out for our information circulars in due course.

We wish to take this opportunity to thank United Nations Malaysia for a timely article on the recently launched UNCTAD’s “The Least Developed Countries Report 2010”. The report outlines the critical issues, challenges and risks faced by these countries and also offers suggestions on how best they can be overcome, including through the South-South cooperation organisations in countries such as Malaysia.

Among ASEAN member countries themselves, there are a number of LDCs which include Lao PDR, Cambodia and Myanmar. We have MASSA members and many other Malaysian corporations already doing business in these countries. In this connection, their business networks, insight and experiences in these countries may provide a better appreciation to navigate the complexities of LDC economies towards a more dynamic, sustainable and equitable growth path for these countries.

As 2010 comes to a close, we wish to express our heartfelt thanks to all members, associates, sponsors and contributors, for assisting us in the publication of MASSA newsletters throughout 2010. We look forward to further assistance and a closer rapport with all of you in 2011 to strengthen and enhance the South-South platform.

We in the Editorial team wish to extend to all members, associates and readers our Best Wishes for the New Year.

Fatimah Sulaiman

Editor

Forthcoming Events

1. Expo Pakistan 2011 at Karachi Expo Center, Pakistan, 25 – 27 February 2011.

2. MASSA Business Mission to Colombia, Ecuador and Venezuela, March/April 2011.

3. Showcase Malaysia 2011 in Dhaka, Bangladesh, 10 – 12 June 2011.

4. MASSA Business Mission to Myanmar, October/November 2011.